What Does Tax Code 1257L Mean? The 2025/2026 UK Guide

Understanding your tax code is the first step toward ensuring your take-home pay is accurate. While 1257L is the most common code for millions of UK employees, it is not a set-and-forget number.

Because the UK Personal Allowance remains frozen at £12,570 through 2026/27, even a small pay rise or a new company benefit can shift your code, potentially triggering an emergency tax status or a tax trap.

The following guide breaks down exactly how to read your payslip and what to do if HMRC changes your status.

What does tax code 1257L mean?

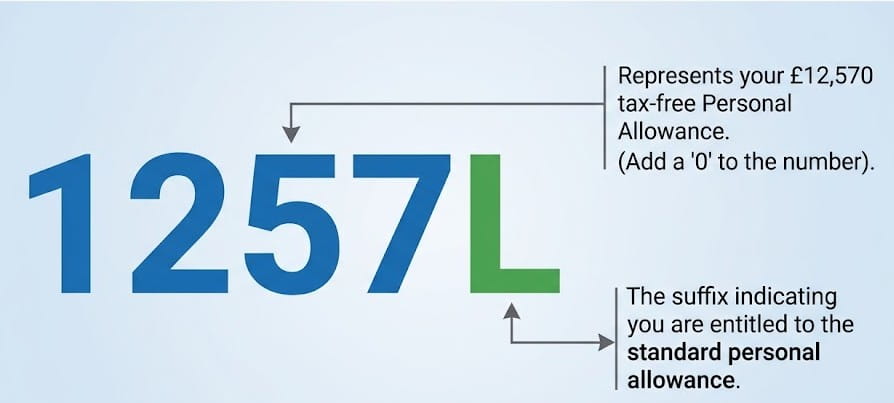

Tax code 1257L is the standard UK tax code for the 2026/27 tax year, indicating a Personal Allowance of £12,570. This is the amount you can earn tax-free annually. The 1257 represents the allowance, while L confirms you are entitled to the standard personal allowance rate.

Your tax code acts as the primary instruction to your employer on how much to deduct from your pay. Under the 1257L code, the first portion of your salary is ignored for tax purposes.

| Pay Frequency | Tax-Free Threshold (1257L) | Typical Income Tax Rate |

| Weekly | £242 | 20% over threshold |

| Monthly | £1,047.50 | 20% over threshold |

| Annually | £12,570 | 20% over threshold |

How do UK tax codes work within the PAYE system?

The PAYE (Pay As You Earn) system divides your £12,570 tax-free allowance across your pay periods. HMRC allocates £1,047.50 monthly or £242 weekly. If earnings exceed these thresholds, your employer automatically deducts Income Tax on the surplus at the applicable 20%, 40%, or 45% tax bands.

| Income Band | Tax Rate | Taxable Income (on 1257L) |

| Personal Allowance | 0% | Up to £12,570 |

| Basic Rate | 20% | £12,571 to £50,270 |

| Higher Rate | 40% | £50,271 to £125,140 |

| Additional Rate | 45% | Over £125,140 |

Note: Income tax rates for England, Wales, and Northern Ireland are currently identical. Scottish taxpayers use different bands (e.g., S1257L).

What do the numbers and letters in 1257L mean?

A tax code breakdown reveals your specific tax status. While 1257L is the most common, referring to a list of tax codes can help you identify if you have been placed on a more specialised code

Significance of other variations

-

L: Standard personal allowance.

-

S: (e.g., S1257L) You are a Scottish taxpayer, subject to Scottish Income Tax rates.

-

C: (e.g., C1257L) You are a Welsh taxpayer.

-

N: You have received a Marriage Allowance transfer from your partner.

What does 1257L W1 or 1257L M1 mean on my payslip?

Suffixes like W1 (Week 1) or M1 (Month 1) indicate an emergency tax code. This means your tax is calculated in isolation for that pay period rather than cumulatively for the year. This typically happens when you start a new job without a P45, leading many to wonder how much emergency tax they will pay on their first paycheck.

-

1257L X: This is often used interchangeably with W1/M1; it means the tax is non-cumulative.

-

1257L Cumul: This confirms your tax is being calculated cumulatively, taking into account all pay and tax to date this year.

-

1257L 0 or 1: These are rarer variations often used during internal payroll transitions or for specific temporary adjustments where a portion of the allowance is restricted.

How to fix an emergency code?

To fix an emergency tax code;

-

Provide your new employer with your P45 from your previous job.

-

If you don’t have a P45, complete the HMRC Starter Checklist.

-

Check your Personal Tax Account via the HMRC website or app.

-

Notify HMRC if you have multiple jobs to ensure the allowance isn’t duplicated.

-

HMRC will then send a digital ‘P6’ notice to your payroll department to fix the issue automatically via your digital payroll records.

-

Verify your next payslip to ensure the W1 or M1 suffix has been removed.

-

Request a refund for any overpaid tax once the correct code is applied.

Why has my tax code changed from 1257L?

Your tax code changes if your Personal Allowance is adjusted due to untaxed income, company benefits, or state pensions. HMRC reduces the 1257L code to collect tax on these benefits in kind, while earners over £100,000 lose their allowance entirely, resulting in codes like 0T or K.

-

The K Code (Negative Allowance): Used when your untaxed income (pensions/benefits) is greater than your Personal Allowance. Effectively, you have minus tax-free pay.

-

Marriage Allowance (1131L): If you transfer 10% of your allowance to a spouse, your code drops to roughly 1131L.

-

Company Benefits: If you have a company car or health insurance, HMRC reduces your 1257L code (e.g., to 950L) to collect tax on these benefits in kind.

-

The 60% Tax Trap: Earners over £100,000 lose £1 of allowance for every £2 earned above that limit. At £125,140, your allowance is zero, and your code changes to 0

How does 1257L affect the self-employed?

For self-employed individuals, the 1257L code represents the first £12,570 of profit exempt from Income Tax. If you are both employed and self-employed, HMRC generally applies the full 1257L allowance to your PAYE employment income first to simplify your tax deductions.

However, staying organised is key, as HMRC can fine households £100 for late self-assessment filings.

Refunds and Reductions

HMRC reconciles overpaid tax at the end of the tax year, often issuing a P800 tax calculation letter. However, you can claim manual refunds faster via the HMRC app if you were on an emergency code. Proactive management ensures you utilize reliefs like pension contributions or Gift Aid to lower liability.

Managing 1257L in Your Payroll Software

Modern software like Xero or QuickBooks updates employee tax codes automatically upon receiving digital P9 notices from HMRC. Small business owners must ensure new hires complete a Starter Checklist to avoid emergency deductions that negatively impact employee take-home pay.

Ways to reduce your Income Tax liability:

- Pension Contributions: Payments into a pension can lower your taxable income; you can also explore strategies on how to avoid paying tax on your pension to maximise your retirement savings.

-

Gift Aid: Charitable donations can provide tax relief for higher-rate payers.

-

Salary Sacrifice: Schemes for cycles or electric cars are deducted before tax.

Manage your 1257L Code

The 1257L tax code is the bedrock of the UK tax system, ensuring the first £12,570 of your earnings remains in your pocket.

-

Check every payslip: Ensure the letter hasn’t changed to W1 or M1 unexpectedly.

-

Claim your expenses: If you wear a uniform or pay professional fees, you can increase your code (e.g., to 1263L) to pay less tax.

-

Review at Year-End: If you were on an emergency code, you might be due a refund. HMRC will send a P800 letter after April, but you can claim faster via the HMRC app.

| Factor | Effect on 1257L Code | Tax Saving Type |

| P60 Reconciliation | None | Overpayment Refund |

| Marriage Allowance | Decreases to ~1131L | Transferable Relief |

| Blind Person’s Allowance | Increases by £3,070 | Additional Allowance |

FAQ about what does tax code 1257l mean?

Is 1257L a good tax code?

Yes, it is the best standard code because it ensures you get the full £12,570 tax-free allowance. If your code is lower (e.g., 1100L) and you don’t know why, you are likely overpaying tax.

How much can I earn on 1257L before paying tax?

You can earn up to £12,570 in a tax year. Weekly, this is approximately £242, and monthly, it is £1,047. Any income above these amounts is subject to deductions.

Does 1257L include National Insurance?

No. The tax code only determines Income Tax. National Insurance (NI) is calculated separately based on different thresholds and is not affected by your tax code.

Can I have 1257L on two different jobs?

Usually, no. HMRC typically applies your full allowance (1257L) to your main job and uses a BR (Basic Rate) or D0 (Higher Rate) code for the second job to avoid underpaying tax.

Why does my payslip say 1257L 0 or 1257L 1?

These are often internal payroll markers. 1257L 0 usually confirms the primary record, while 1257L 1 might indicate a secondary pay stream within the same company. They function exactly like the standard 1257L.

Is 1257L 20%?

1257L itself is the allowance. Once you exceed £12,570, the income that follows is taxed at 20% until you reach the higher rate threshold.

How do I check if my tax code is correct?

You should compare your code against your actual circumstances using the Check your Income Tax service on the GOV.UK website.