Statement of Financial Position: A UK Small Business Guide

A statement of financial position provides an immediate, clear snapshot of a business’s total assets, liabilities, and equity at a specific point in time.

For business owners, creditors, and stakeholders throughout the UK, it serves as a fundamental, day-to-day diagnostic tool for tracking long-term corporate solvency, liquid capital availability, and overall financial health.

What is the statement of financial position?

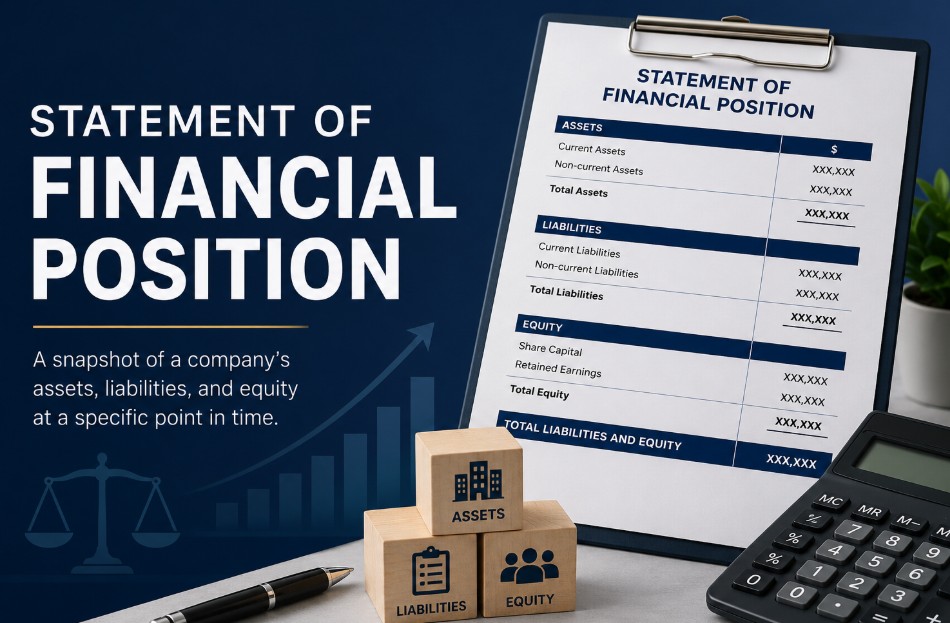

A statement of financial position is a formal accounting document that summarizes a company’s financial status by detailing its assets, liabilities, and equity at an exact point in time.

It follows the fundamental accounting equation where Total Assets must perfectly equal the sum of Total Liabilities and Shareholders’ Equity.

The document functions as an official record of what a business owns and owes at the close of an accounting period. By anchoring the business’s books to a fixed mathematical balance, it provides an objective view of its structural net worth.

Truths of Financial Reporting

Unlike the income statement, which captures performance over a duration, this report functions as a static image. It isolates the financial reality of the business on a specific date, typically the end of a financial year.

Understanding this distinction is vital for accurate bookkeeping, as it separates operational profit from long-term capital structure.

Is a statement of financial position a balance sheet?

Yes, a statement of financial position is the modern, official regulatory name for a traditional balance sheet.

While the terms are used interchangeably in daily UK business, statement of financial position is the required term under international standards adopted by modern UK accounting frameworks.

Under the Companies Act 2006 and modern UK financial reporting frameworks like FRS 102, the traditional term has evolved to be more descriptive.

However, the underlying accounting components, assets, liabilities, and equity, remain entirely identical to traditional balance sheet practices used by generations of UK accountants.

Statement of Financial Position vs Balance Sheet Comparison

The comparison between a statement of financial position and a traditional balance sheet reveals that they contain identical financial data and serve the same statutory function for Companies House filings, differing only in their historical terminology.

-

Terminology: Statement of financial position is the standard modern IFRS and FRS 102 label, while balance sheet remains the popular legacy term.

-

Content: Both documents track the exact same core elements: Assets, Liabilities, and Shareholders’ Capital.

-

Reporting: Both fulfill the identical regulatory requirement for filing annual statutory accounts in the UK.

Key Differences and Similarities

The key differences between financial statements lie in their time horizons and core equations, while their primary similarity is that they link together at year-end to show how operational trading changes a company’s total net worth.

The table below outlines how these two primary statutory documents interact and differ under UK reporting rules:

| Feature | Statement of Financial Position | Income Statement (Profit & Loss) |

| Core Purpose | Shows the structural status of assets and liabilities | Shows operational revenue, costs, and net profit or loss |

| Timeframe | Static snapshot calculated at a specific year-end date | Dynamic performance tracking over an entire accounting period |

| Governing Equation | Assets = Liabilities + Shareholders’ Equity | Revenue – Expenses= Net Profit or Loss |

Understanding the Statement of Financial Position Format

The standard format of a statement of financial position is structured hierarchically by liquidity, placing long-term fixed assets at the top, followed by short-term current assets, immediate current liabilities, long-term liabilities, and ending with shareholders’ equity at the base.

This specific layout helps external readers, such as banks or suppliers, instantly analyze how quickly a company’s resources can be turned into liquid cash and how urgently its outstanding debts must be settled.

Components of the Statement of Financial Position

A classified statement of financial position groups items by their nature and liquidity (how quickly they can be turned into cash). This helps readers understand the urgency of liabilities and the availability of resources.

The document is systematically divided into three core pillars, broken down into current and non-current categories:

-

Non-Current Assets: Long-term investments, property, plant, machinery, vehicles, and intangible assets (like trademarks) that the business intends to keep for longer than 12 months.

-

Current Assets: Short-term resources expected to be realized, sold, or consumed within the upcoming year. This includes inventory (stock), trade receivables (trade debtors), and cash at the bank.

-

Current Liabilities: Debts due for payment within 12 months, such as trade creditors, short-term overdrafts, and immediate HMRC tax provisions.

-

Non-Current Liabilities: Long-term financial commitments that extend beyond one year, including mortgages, director loans, or long-term bank financing.

-

Shareholder Equity: Positioned at the base of the report, this represents the net worth belonging to the owners, calculated by deducting total liabilities from total assets. It includes original share capital and accumulated retained earnings.

Purpose of Statement of Financial Position in UK Business

The primary purpose of a statement of financial position in UK business is to provide complete financial transparency regarding a company’s short-term liquidity and long-term solvency to external stakeholders, lenders, and HMRC.

By publishing this document annually, an enterprise provides concrete proof to the market that it possesses a healthy balance of resources to back up its commercial trading activities.

Indicators of Business Health

The three primary indicators of business health derived from a statement of financial position are liquidity (short-term bill-paying capacity), solvency (long-term debt survival), and capital structure (the balance of debt versus equity funding).

-

Liquidity: The day-to-day ability to settle pressing short-term debts using immediately available cash or near-cash equivalent assets.

-

Solvency: The ultimate long-term capacity of an enterprise to meet its global financial obligations as they fall due over several years.

-

Capital Structure: The ratio showing how much of the business is funded by external debt liabilities versus internal shareholder investment capital.

How to use the Statement of Financial Position?

To use a statement of financial position effectively, business owners and investors must calculate specific financial ratios from its figures to evaluate a company’s immediate cash safety margins and its structural stability against market changes.

Interpreting the raw figures turns a compliance document into a practical diagnostic map for running vital financial health checks.

Conducting Liquidity Analyses

You can use the figures to see if the business can cover its immediate debts. By comparing current assets to current liabilities (the Current Ratio), you get a clear indication of short-term cash safety.

Assessing Solvency and Leverage

By comparing external debt against internal shareholder investment (Capital Structure), stakeholders evaluate long-term financial stability. A business heavily reliant on long-term loans may face higher risks if interest rates fluctuate or market conditions tighten.

Tracking Internal Synergy with the Income Statement

These documents are intrinsically linked. The profit or loss calculated in your income statement at the end of the year is transferred directly to the equity section of your statement of financial position as retained earnings.

-

Net Profit increases equity and consequently boosts net assets.

-

Net Losses or dividend payments directly reduce equity, signaling a decline in overall business book value.

Why is Statement of Financial Position important?

The statement of financial position is important because it serves as the ultimate proof of creditworthiness for securing bank capital, ensures strict tax compliance with HMRC asset classification standards, and provides the baseline data required for long-term strategic expansion planning.

In the competitive UK marketplace, it is a vital tool for forward-looking strategic decision-making.

-

Securing Credit and Capital: Banks, suppliers, and peer-to-peer lenders will scrutinize this statement before approving business loans or trade credit terms to determine creditworthiness.

-

Tax Compliance and Accuracy: It ensures your asset valuations are compliant with HMRC reporting standards, protecting small businesses from costly categorisation errors (such as mistakenly misclassifying a major capital expenditure asset as a temporary revenue repair expense).

-

Strategic Planning: It provides business owners with the data needed to make informed choices regarding expansion, debt restructuring, and timing asset purchases.

Pros and Cons for Statement of Financial Position

The main pro of a statement of financial position is that it provides a standardized, objective benchmark of a company’s net worth, while its main con is its historical bias, meaning it only reflects past transactions rather than current real-world market values.

Understanding both sides ensures you don’t over-rely on a single document during commercial planning.

| Pros | Cons |

| Objective Benchmark: Gives a standardized, universally understood picture of corporate net worth according to FRS 102 rules. | Historical Bias: Reflects past transactions; book values of assets like property or equipment may not match current market values. |

| Highlights Vulnerabilities: Clearly exposes structural issues, such as dangerous levels of short-term debt or slow-moving stock ties. | No Context on Cash Timing: Lists static cash balances but fails to show the immediate day-to-day timing of cash coming in or going out. |

| Aids Investor Valuation: Simplifies corporate analysis and the calculation of essential financial metrics like Return on Equity (ROE). | Omission of Intangible Value: Critical elements like brand loyalty, staff expertise, and intellectual property are rarely captured, understating actual worth. |

How to prepare a statement of financial position?

To prepare a statement of financial position, you must systematically reconcile all ledger accounts, list and categorize all assets and liabilities into current and non-current brackets, calculate shareholders’ equity, and verify that the final figures satisfy the equation: Assets = Liabilities + Equity

The preparation process requires a step-by-step methodology to ensure compliance with UK regulatory frameworks.

-

Gather all bank statements and reconciled ledger balances for the year-end date.

-

List all non-current assets, such as machinery, property, and intangible assets.

-

Calculate total current assets, including inventory, trade receivables, and cash at bank.

-

Identify all current liabilities, such as trade creditors and short-term loans.

-

Determine long-term liabilities, including mortgages or long-term bank financing.

-

Calculate shareholder equity by deducting total liabilities from total assets.

-

Verify that the final figures satisfy the fundamental accounting equation.

-

Review the document against regulatory requirements to ensure compliance with FRS 102.

Managing Categorisation Errors

Managing categorization errors requires carefully distinguishing between capital expenditure (adding a long-term asset to the statement of financial position) and revenue expenditure (recording an immediate repair cost as an expense on the income statement).

Final Summary

The statement of financial position is more than a compliance requirement; it is a vital diagnostic tool for any UK business. By reviewing assets against liabilities regularly, owners can make informed strategic decisions regarding expansion, debt management, and cash flow.

Next, ensure your choice of the best small business accounting software is properly configured to produce this report automatically in line with FRS 102 standards, and consult with a qualified accountant to interpret the ratios for your specific industry.

FAQ

What are the 4 basic financial statements?

The four basic statements are the statement of financial position, the income statement, the statement of cash flows, and the statement of changes in equity. Together, they provide a comprehensive view of business performance.

What is another name for statement of financial position?

The document is most commonly referred to as a balance sheet. In specific academic or international accounting contexts, it may also be described as a statement of net worth or position statement.

What are the 5 elements of a financial statement?

The five core elements are assets, liabilities, equity, income, and expenses. These categories encompass every financial transaction and position recorded within a business’s accounting system during a given period.

What is the purpose of a consolidated statement of financial position?

A consolidated version combines the financial position of a parent company and its subsidiaries into a single report. It provides stakeholders with a holistic view of the entire corporate group’s financial status.

How do I find a statement of financial position template?

Many accounting software providers offer pre-built templates. Alternatively, reputable UK accountancy bodies such as the ICAEW provide guidance and example formats that align with current FRS 102 regulatory standards for small entities.

Why is a classified statement of financial position important?

Classification separates assets and liabilities into current and non-current categories. This is essential for calculating liquidity ratios, helping owners understand if they can cover immediate debts without liquidating long-term assets.

What are the three major types of financial position assessments?

The three assessments include liquidity analysis (short-term cash health), solvency analysis (long-term debt capacity), and efficiency analysis (how well assets are utilised to generate profit within the business operations).