I have never paid National Insurance will I get a pension? (2026/27 Guide)

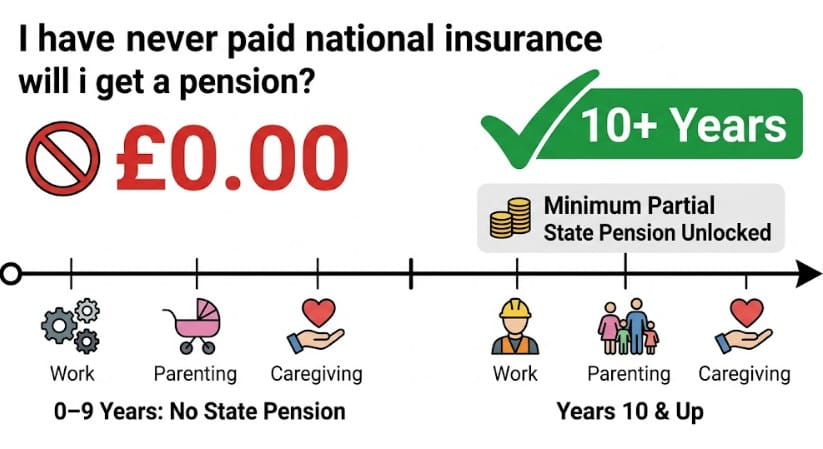

If you are approaching retirement and realise your National Insurance (NI) record is empty, you are likely asking: I have never paid National Insurance will I get a pension? The short answer is no, you cannot claim the standard UK State Pension without at least 10 qualifying years.

Individuals asking I have never paid National Insurance will I get a pension should know that while a standard UK State Pension requires 10 qualifying years, those with empty records can safely claim Pension Credit. This safety net benefit guarantees a baseline weekly retirement income for low-income UK residents.

Reaching retirement age without a standard work history is a common concern, but your ultimate financial outcome depends on more than just your payslips.

Whether you can claim a payment often hinges on hidden credits from years spent raising a family or your eligibility for the UK’s low-income safety net.

The Rule of 10: I have never paid National Insurance will I get a pension?

To receive any New State Pension in the UK, you must have a minimum of 10 qualifying years on your National Insurance record. If you have zero years, you will not receive a State Pension payment.

Fortunately, you are not left with nothing. If you live in the UK and have a low income, you can claim Pension Credit instead.

According to official Department for Work and Pensions (DWP) guidelines for the 2026/27 tax year, this safety net tops up your weekly income to a minimum of £238.10 (for single people) or £363.00 (for couples), effectively providing a pension-level income regardless of your NI history.

Gaining a clear understanding of your eligibility requires you to distinguish between paying National Insurance out-of-pocket and accruing qualifying years through credits.

-

The Minimum Threshold: You need 10 years for a partial pension.

-

The Full Pension: You need 35 years for the full New State Pension of £241.30 per week.

-

Qualifying via Credits: Many people who never paid NI actually have qualifying years through automatic credits (e.g., raising children, being a carer, or claiming certain benefits).

The threshold for receiving a retirement income

Under the current system, having fewer than 10 years results in a zero-value State Pension. However, it is a common pattern for people to assume they have no record when, in fact, they have accrued years through the benefit system.

For example, a parent who stayed home to raise a child under the age of 12 and claimed Child Benefit will have automatically received National Insurance credits that count toward this 10-year minimum. Figures released by the DWP confirm that these small credits fully establish baseline pension metrics.

| NI Qualifying Years | State Pension Payout Estimates for 2026/27 | Status |

| 0 to 9 Years | £0.00 | No State Pension entitlement |

| 10 Years | £68.94 | Minimum partial State Pension |

| 20 Years | £137.89 | Partial State Pension |

| 35 Years | £241.30 | Full New State Pension |

How many NI years do I need for a full pension in 2026?

To claim the full New State Pension, you generally need 35 qualifying years of National Insurance contributions or credits. For the 2026/27 tax year, the full rate is set by the DWP at £241.30 per week, with lesser records paying out on a proportional, pro-rata basis.

Key Fact: The DWP requires a minimum of 10 qualifying years on your record to receive any portion of the standard State Pension. Anything less results in a £0.00 baseline award, making alternate safety nets like Pension Credit necessary.

If your record has gaps, your weekly payment is reduced proportionally, provided you have met the initial 10-year threshold mentioned above.

If you are unsure where you stand, you can follow these practical steps to identify and fill any gaps in your record:

-

Request a State Pension Forecast: Access the Check your State Pension service on GOV.UK to see your current year count.

-

Identify Gaps: Review your National Insurance record to find years that are not full.

-

Check for Missing Credits: Ensure you claimed credits for periods of caregiving or unemployment.

-

Verify Eligibility to Buy: Confirm if you are eligible to pay Class 3 voluntary contributions for the missing years.

-

Calculate the Cost: Determine if the cost of the voluntary payment (approx. £956.80 for a full year in 2026) outweighs the pension increase.

-

Make Payment: Use the HMRC online service or pay via bank transfer to fill the selected gaps.

-

Confirm Update: Check your record after 8 weeks to ensure the years are now marked as full.

How do I know if I am entitled to a UK pension?

Entitlement is determined by your National Insurance record and your age. As of 2026, the State Pension age is 66, though it is gradually transitioning toward 67.

Those in the public sector might have different rules to consider, such as the NHS pension after 20 years, which operates independently of the basic State Pension requirements.

You can verify your status by viewing your National Insurance record online through the Personal Tax Account. This digital statement lists every year since you turned 16 and specifies whether that year counts toward your pension.

Identifying your qualifying status

A common mistake occurs when individuals confuse working years with qualifying years. It is a frequent oversight to equate employment with pension eligibility.

Many people who have never held a traditional job, such as registered foster carers or those on Carer’s Allowance, are surprised to find they have already built a substantial National Insurance record through automatic credits.

-

Child Benefit: Credits for parents/guardians of children under 12.

-

Carer’s Credits: For those spending 20+ hours a week looking after someone with a disability.

-

Specified Adult Childcare Credits: For grandparents moving credits from a working parent.

-

Statutory Sick Pay: Periods where you were unable to work due to health issues.

What happens if I have less than 35 years of National Insurance?

If you reach State Pension age with between 10 and 34 qualifying years, the DWP awards you a reduced pro-rata pension. This payment scales linearly based on your exact year count; for example, holding 25 qualifying years secures you exactly 25/35ths of the full weekly entitlement.

To help separate misunderstandings from legal reality regarding thin NI contribution profiles, consider this breakdown:

| Myth regarding zero NI records | Reality under official DWP frameworks |

| Never working means you get zero income at age 66. | False. Pension Credit guarantees low-income individuals a baseline weekly income regardless of work history. |

| You can only get NI years if you pay tax on a salary. | False. Free National Insurance credits are granted for childcare, caregiving, and health conditions. |

| Missing the 10-year mark means your retirement options are gone. | False. You can often buy back missing gap years via voluntary Class 3 HMRC payments to unlock the pension. |

This calculation is performed automatically by the Department for Work and Pensions (DWP) when you reach the eligible age and make a claim.

Hidden Ways You Might Have Earned Credits Without Knowing

Many people who believe they have never paid National Insurance actually have qualifying years on their record.

This happens through National Insurance Credits, years that the government gives you for free because of your life circumstances.

-

Time Spent Raising Children: If you claimed Child Benefit for a child under 12, you likely earned automatic credits.

-

Caring for Family or Friends: If you spent 20 hours or more a week looking after someone with a disability, you may have earned Carer’s Credits.

-

Grandparents Providing Childcare: You can actually transfer credits from a working parent to a grandparent who is helping with the kids.

-

Illness and Disability: If you were unable to work due to a long-term health condition, you may have been awarded credits during that time.

Should You Spend Money to Buy Back Missing Years?

Buying voluntary Class 3 National Insurance contributions allows individuals to fill gaps in a thin record. According to HMRC, purchasing a full missing year costs roughly £956.80 in 2026, a move that can successfully lift you past the mandatory 10-year state pension threshold.

Checking your record to discover you hold 8 or 9 years places you in a structural danger zone. Missing that 10-year mark by just one single year means you get nothing from the standard State Pension fund.

Buying Voluntary Contributions: It currently costs about £956.80 to buy one full year of National Insurance via HMRC frameworks.

Is it worth it? Usually, yes. Reaching that 10-year milestone can turn a £0 pension into thousands of pounds over the course of your retirement.

A Word of Caution: If you are already eligible for the full Pension Credit top-up, buying NI years might not actually increase your total income. It is always best to speak to a specialist before spending your savings on buy-backs.

For individuals who sit just a few years short of the 10-year threshold, making these specific payments can unlock a lifetime of structural State Pension payouts that would otherwise equal zero.

As you plan your retirement income, you should also look at ways to avoid tax on your pension to ensure you keep more of the money you’ve secured.

However, if you are eligible for Pension Credit, buying years might be unnecessary as the credit would simply top up your income to the same level.

Can I pay voluntary NI contributions if I live abroad?

Yes, UK citizens or former residents living overseas can often pay voluntary contributions to maintain their record.

Depending on your employment status abroad, you may qualify for Class 2 contributions, which are significantly cheaper than the standard Class 3 rates.

This is a vital strategy for expats who intend to return to the UK or wish to claim their UK pension while residing in another country.

How much is Pension Credit for those with no NI?

Pension Credit acts as a critical safety net for UK residents with no National Insurance history. In 2026, this means-tested benefit tops up your weekly income to a guaranteed minimum of £238.00 for singles or £363.25 for couples, ensuring financial security even with zero years of contributions.

It is a means-tested benefit that tops up your weekly income to a guaranteed level; however, many individuals are unsure of their eligibility for the Guaranteed Pension Credit or whether they meet the specific income thresholds.

- Passported Benefits: Claiming Pension Credit often unlocks extra help, including Housing Benefit, Council Tax reduction, and the free TV license for those over 75.

Pro Tip: Even if you are only entitled to £1 of Pension Credit, you should claim it. It is the gateway to thousands of pounds in additional cost-of-living support.

| Feature | State Pension | Pension Credit |

| Basis | Contributions (NI Years) | Financial Need (Means-tested) |

| Minimum Years | 10 Years | 0 Years |

| 2026 Rate (Single) | Up to £241.30 | Up to £238.10 (Guarantee) |

| Extra Benefits | None automatically | Includes Housing Benefit & Council Tax help |

How to Claim Pension Credit with No National Insurance?

You can secure your income even with a zero-year record by following a few simple steps. Because this is based on need, the DWP focuses on your savings and current income rather than your work history.

What do you need to apply?

-

Your National Insurance Number: Even with zero contributions, you still have this unique ID.

-

Financial Details: Have information ready regarding any savings, investments (over £10,000), or other benefits you receive.

-

Bank Details: Where you want your weekly support to be paid.

The Easiest Ways to Apply

-

Online: Visit GOV.UK, if you have already reached the qualifying age.

-

By Phone: Call the Pension Credit claim line on 0800 99 1234. This is often the best route if you need a staff member to walk you through the questions.

-

By Post: You can request form PC1 be sent to your home address.

Pro Tip: You can apply up to four months before you reach State Pension age. If you apply late, you can ask for the claim to be backdated by three months.

Summary of Next Steps

If you are worried about a thin National Insurance record, your first step should be to get a clear picture of your current standing. Logging into the Government Gateway for a formal forecast will remove the guesswork and show exactly where you stand.

Before assuming you have zero years, check for National Insurance Credits. You may have accrued years automatically if you were:

-

Raising Children: Claiming Child Benefit for a child under 12 provides automatic NI credits.

-

A Carer: If you spent 20+ hours a week caring for someone, you might have Carer’s Credits.

-

Grandparenting: Specified Adult Childcare Credits allow working parents to transfer their NI credits to a grandparent who is looking after the child.

Before applying, it is vital to understand the limits on pensioner savings, as your capital can impact your eligibility for means-tested support.

Ultimately, resolving the question of I have never paid National Insurance will I get a pension?” means identifying hidden credits or securing mean-tested DWP safety nets for low-income retirees in the 2026/27 period.

FAQ: I have never paid National Insurance will I get a pension?

Can I get a pension at 67 with 0 years?

No, you cannot receive the State Pension with zero NI years. However, you should apply for Pension Credit, which provides a similar weekly income for those on low incomes, regardless of their NI record.

What is the biggest mistake most people make regarding retirement?

The most significant error is failing to check their NI record before reaching age 60. Many people have gaps that they could have filled for free via credits or low-cost voluntary payments while they still had time.

How much state pension will I get at 66?

If you have 35 qualifying years, you will receive £241.30 per week. If you have 10 years, you receive £68.94. With fewer than 10 years, you receive nothing from the State Pension fund.

What is the new pension age in the UK?

The current State Pension age is 66 for both men and women. It is scheduled to rise to 67 between 2026 and 2028, depending on your date of birth.

What happens to my pension if I quit my job?

Quitting does not delete your previous contributions. Your record remains frozen until you earn again, claim credits, or reach pension age. However, stopping work early may leave you with a partial pension if you haven’t hit 35 years.

Can I retire at 62 and get the State Pension in England?

While you can choose to stop working at 62, the state won’t begin your payments until you reach the official qualifying age. For most people in 2026, this means bridging a four-year gap using private savings or other benefits before the State Pension kicks in.

How much is the State Pension for a woman?

Under the New State Pension system introduced in 2016, men and women are treated exactly the same. Your payment depends entirely on your National Insurance record, not your gender.

Can my spouse’s National Insurance record give me a State Pension?

No, under the New State Pension rules introduced in 2016, you cannot inherit or build a baseline entitlement using your spouse or civil partner’s National Insurance contribution history. Your application depends entirely on your own personal account history and accumulated credits.

Does owning a house stop me from getting Pension Credit if I have no NI?

No, owning the home you actively live in does not disqualify you from receiving income support. The DWP evaluates your weekly income and any capital/savings over £10,000, but the physical property of your primary residence is excluded from the calculation.

Can I get a free TV licence if I have never paid National Insurance?

Yes, provided you are aged 75 or over and successfully claim Pension Credit to support your household. Because Pension Credit does not require an employment history, it acts as the gateway to receiving a free TV licence regardless of your historical NI contributions.

Will receiving an inheritance cancel my Pension Credit safety net?

Yes, it can if the inherited cash lump sum drives your total personal savings threshold above the permitted limits. While capital under £10,000 does not affect your Pension Credit, every £500 you possess over that threshold counts as a deemed weekly income asset, and significant windfalls will terminate means-tested benefit structures entirely.