HMRC Pensioner Bank Deduction £420: Why is it Happening in 2026?

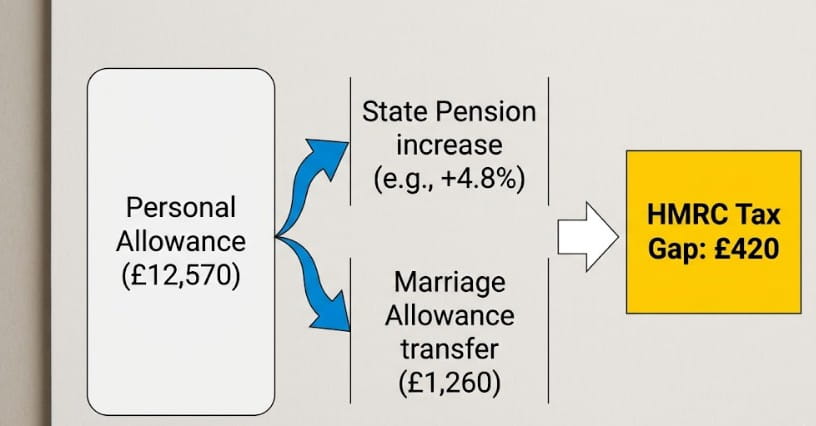

An HMRC pensioner bank deduction £420 is a tax reconciliation payment triggered when a retiree’s total income exceeds the frozen £12,570 Personal Allowance. In 2026, this specific £420 figure typically results from a Simple Assessment (PA302) tax bill or a 20% basic rate charge on roughly £2,100 of excess income following the 4.8% State Pension triple-lock increase.

This specific figure often represents a reconciliation of underpaid tax where HMRC cannot collect the balance through standard monthly PAYE deductions.

Why has HMRC deducted £420 from my pension?

An HMRC pensioner bank deduction £420 usually occurs when HMRC identifies an underpayment of tax that cannot be recovered through your monthly pension payments.

This often happens if you have claimed backdated Marriage Allowance or if the 2026 State Pension increase pushed your total annual income above the £12,570 threshold for the first time.

A deduction of exactly £420 often stems from a backdated Marriage Allowance claim or a reconciliation of underpaid tax from a previous year.

When the lower-earning spouse transfers £1,260 of their Personal Allowance, it creates a tax saving for the recipient; however, if the claim is backdated or if a Simple Assessment is triggered for the 2024/25 tax year, the resulting bill frequently lands in this specific price range for those with small private pensions.

Evidence from the 2025/26 tax year suggests that the ‘catch-up’ effect of the State Pension rising by 4.8% has left many retirees with an unexpected tax gap.

If your total income exceeded the £12,570 threshold and HMRC could not collect the tax via your monthly PAYE code, they would issue a demand for the lump sum.

Similar deductions of £300 or £500 are also common for those whose tax codes (such as the 1131L code) were adjusted mid-year to account for benefits or untaxed interest.

Common Reasons for Pension Deductions in 2026

If you see a deduction of exactly £420, it is usually not a mistake or a bank error. It is a calculated recovery of underpaid tax. In 2026, there are three primary reasons for this specific amount:

-

The State Pension Catch-Up: With the Personal Allowance frozen at £12,570 and the State Pension rising by 4.8% this April, many retirees are crossing the tax threshold for the first time. A £420 bill often represents the tax due on a small private pension that HMRC couldn’t collect via standard PAYE.

-

Backdated Marriage Allowance: If you or your spouse recently cancelled or adjusted a Marriage Allowance claim, HMRC may issue a demand to recover the £1,260 allowance transfer, which, at the 20% basic rate, equals a reconciliation in this price bracket.

-

Simple Assessment (Form PA302): If your income is too complex for a standard tax code to handle, HMRC issues a Simple Assessment. This is a one-off demand for the tax year rather than a monthly deduction.

Check your 1131L tax code. If you see this on your statement, it means your tax-free threshold has been reduced by £1,260, often leading to a calculated underpayment of roughly £420 over the year.

How was the £420 deducted from my pension?

HMRC deducts the £420 via two primary methods: Deduction at Source through your pension provider (PAYE) or a Simple Assessment (PA302) payment. Most pensioners see this as a reduced monthly payout because HMRC adjusted their tax code (e.g., 1131L) to collect underpaid tax automatically before the funds reach their bank account.

Mechanically, this deduction happens through three specific channels:

-

The PAYE System: HMRC sends a digital P6 coding notice to your pension provider (like the DWP or a private fund). They then withhold the tax directly from your gross pension.

-

Simple Assessment (PA302): If you only receive the State Pension, HMRC cannot tax the DWP directly. Instead, they send you a PA302 letter demanding the £420, which you pay via the HMRC app or bank transfer.

-

Tax Code Adjustments: If your code changed to 1131L, your tax-free allowance was slashed by £1,260. At the 20% basic rate, this results in exactly £252 of Marriage Allowance recovery plus potential interest, often totalling near the £420 mark.

Can HMRC take money directly from my bank account?

No, HMRC cannot simply dip into your savings without notice. While they hold Direct Recovery of Debts (DRD) powers, these are reserved for debts over £1,000 and require a 30-day warning period.

For most, the HMRC pensioner bank deduction £420 is not a direct withdrawal from a bank account but rather a deduction made by your pension provider before the money reaches you, or a request for you to pay a Simple Assessment bill via bank transfer.

A common pattern is for HMRC to send a warning letter at least 30 days before taking any enforcement action. To use DRD, the tax debt must be over £1,000, and the debtor must have been contacted multiple times.

What you are seeing as a bank deduction is almost always one of two things:

- A Deduction at Source: Your pension provider (like DWP or a private fund) deducted the tax before it reached your bank.

- A Simple Assessment Payment: You may have a standing order or a manual payment triggered by a P800 or PA302 letter you received.

Therefore, if you see a £420 deduction, it is almost certainly a tax code change (PAYE) rather than a direct seizure of funds.

How to Resolve an HMRC Deduction Issue?

-

Log in to your Personal Tax Account (PTA) on the official GOV.UK portal.

-

Check your current Tax Code (e.g., 1257L, 1131L, or a ‘K’ code).

-

Compare the Income from Pensions section with your actual bank statements.

-

Review any P800 Tax Calculation or Simple Assessment letters received in the post.

-

If the figures are incorrect, use the HMRC digital assistant to flag an error.

-

Call the Income Tax Helpline (0300 200 3300) specifically on Tuesday or Wednesday mornings for faster service.

If you are owed money back, you can check the typical HMRC tax refund wait times. It is also vital to stay compliant, as late self-assessment fines of £100 can apply if your total income triggers a formal return requirement.

How do HMRC check my savings?

As of 2026, HMRC uses an automated AI system called ‘Connect’. UK banks and building societies are legally required to report the total interest you earn annually.

Under the Common Reporting Standard, financial institutions must flag any interest that exceeds your Personal Savings Allowance (£1,000 for basic-rate taxpayers). This data allows HMRC to collect tax on savings automatically by adjusting your annual tax code.

| Account Type | 2026 Tax-Free Limit | HMRC Visibility |

| ISA (Cash/Stocks) | £20,000 Annual Deposit | High (but tax-exempt) |

| Standard Savings | £1,000 Interest (Basic Rate) | Fully Reported by Bank |

| Personal Pension | £60,000 Annual Allowance | Fully Reported |

| State Pension | Taxable Income | High (Internal DWP Data) |

What triggers HMRC to check bank accounts more deeply is usually a significant discrepancy between your declared lifestyle and the data provided by banks.

If your interest exceeds the £1,000 Personal Savings Allowance, HMRC will automatically adjust your tax code for the following year to collect that tax, which often results in an unexpected deduction from your monthly pension.

How much money can a pensioner have in the bank before tax?

In the UK, there is no limit on the amount of capital you can hold in a bank account, but there are strict limits on the interest you can earn tax-free.

For 2026, most pensioners can keep roughly £20,000 to £30,000 in a high-interest savings account (at 4-5% interest) before they hit the £1,000 Personal Savings Allowance. Once your interest exceeds this, HMRC will typically reduce your Personal Allowance, leading to a smaller monthly pension.

If you are claiming Pension Credit, the rules change significantly. You can have up to £10,000 in savings without it affecting your benefit payments. Every £500 you have above that £10,000 limit counts as £1 of assumed income per week, which reduces your Pension Credit eligibility.

Essential Savings Facts for Pensioners

-

Maximising your ISA allowance is a vital strategy; you can hold significant savings within an ISA (subject to the £20,000 annual deposit limit) without ever being liable for tax on the interest.

-

The £10,000 Threshold: Keeping more than £10,000 in a standard savings account is perfectly legal, but it does act as a ‘flag’ for HMRC to check that the resulting interest hasn’t exceeded your tax-free allowance.

-

Cash Deposits: While you can deposit large amounts of cash, banks are legally required to ask for the Source of Wealth for deposits over £5,000 to £10,000 to comply with anti-money laundering regulations.

Summary of Next Steps

Discovering an HMRC pensioner bank deduction £420 on your statement is understandably startling, but it almost always points to a specific, fixable tax reconciliation rather than a banking error.

Should the deduction occur via your pension provider, verify your 2026/27 tax code on your latest payslip. Residents who believe a calculation is based on outdated savings figures should update their details through the GOV.UK Personal Tax Account to prevent further monthly losses.

FAQ about HMRC pensioner bank deduction £420

Is the HMRC pensioner bank deduction £420 a scam?

If you receive a text or email asking you to click a link for a £420 refund or to pay a deduction, it is a scam. Official HMRC bank deductions are handled through your pension provider or requested via an official PA302 letter sent to your home address.

Why did my tax code change to 1131L?

The 1131L code usually means your Personal Allowance has been reduced by £1,260. This often happens if you have transferred your Marriage Allowance to a spouse or if HMRC is recovering a previous underpayment.

Can I deposit a large amount of cash in a bank?

Yes, but for amounts over £10,000, the bank must report the transaction. You should keep receipts or legal documents (like a house sale or inheritance letter) to prove the source of the funds.

Does HMRC check my bank account every month?

No. HMRC receives an annual summary from your bank regarding the total interest earned. They do not have live access to your daily transactions unless you are under a formal tax investigation.

How long does a tax refund take in 2026?

If you are owed a refund after an HMRC pensioner bank deduction £420, it usually takes 5 to 10 working days for a bank transfer via the HMRC app. While reviewing your tax position, you may also be eligible to claim mileage from HMRC if you use a personal vehicle for business or certain volunteer roles.

What happens if I don’t declare my savings interest?

HMRC will eventually find out through their automated Connect system. They will then issue a backdated tax bill plus interest and potential penalties for failing to notify.

Will my 2026 State Pension increase be taxed?

Yes, if your total income (including private pensions) exceeds £12,570. The 4.8% increase in April 2026 is a common trigger for these new HMRC deductions.